On 28 March 2022, the Thai Revenue Department (“TRD”) published a Notification of Ministry of Finance regarding TPDF filing deadline extension for FY 2020. Moreover, the TRD also recently issued additional explanation and Q&A for the Transfer Pricing Disclosure Form (“TPDF”) on its TRD website. We have summarised key points as follows:

TPDF filing deadline extension

For the fiscal year beginning from 1 January 2020 to 31 December 2020, the TPDF filing due date has been extended from 150 days after the year-end to 30 May 2022. Additional 8 days of extension for online filing are allowed for taxpayers whose TPDF filing due date falls between 23-30 May 2022.

Additional explanation for TPDF

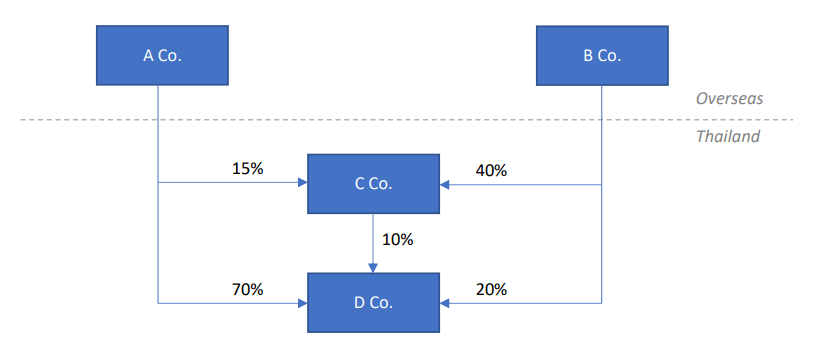

The TRD has updated additional details on the explanation for TPDF by adding example 12 in the appendix (as illustrated below). If a company or juristic partnership with the same group of shareholders holds together at least 50% of the direct shares in one company and at least 50% of the shares in another company, both companies are regarded as related parties under Section 71 bis Clause 2 (2) of the Thai Revenue Code (“TRC”).

C Co. and D Co. are related parties because A Co. and B Co. are shareholders of both companies. A Co. and B Co. directly hold 55% of C Co.’s shares combined, and A Co. and B Co. directly hold 90% of D Co.’s shares combined.

Q&A for the TPDF

We summarise key points for filling information in the TPDF as follows:

Entities obligated for TPDF filing

- The consideration of related parties is still based on the definition from Clause 2 (1) and (2) of Section 71 bis of the TRC. The definition per Section 71 bis Clause 2 (3) has not been announced yet.

- Joint ventures are required to prepare and submit the TPDF if they meet the revenue threshold as well as the related party definitions.

- If the permanent establishment of a foreign juridical company or partnership has revenue of at least THB 200 million during the accounting period and has related parties based on the definitions in Section 71 bis, it is obligated to file the TPDF.

- If a company or juristic partnership established under foreign law has operated a business in Thailand that generates “Business Profit” under a Double Tax Agreement (“DTA”) (no other income) but has no permanent establishment in Thailand under the DTA, it has no duty to file the TPDF.

Filling information in the TPDF (part A – C)

- The taxpayer is required to disclose a list of all related parties in the TPDF, regardless of whether the taxpayer had any transactions with such parties in that accounting period or not.

- Transactions that are not required to be included in the TPDF part B are such as dividend payments, product deposits, depreciation.

- The taxpayer is required to fill in the reimbursement only when it is marked-up while the reimbursement without a mark-up is not required to be disclosed in the TPDF.

- If an entity applies TFRS 16 for asset rental, the amount of the right to use the asset should be disclosed in the Purchase of Property, Plant and Equipment (“PPE”) column only for the first year of recognition and the amount of interest expense should be disclosed in the Other Expense column.

- In respect of intercompany loan transactions for the purchase of assets from third parties, if the assets are not ready for use, the interest expense should be included in the Purchase of PPE column. If the assets are ready for use, the interest expense should be included in the Interest Expense column.

- If purchases of raw materials or goods are part of the Cost of Goods Sold, it should be disclosed as “Purchase of Raw Materials/Good”. If not, it should be disclosed in the “Other” sub-column of the “Other Expenses” column.

- A Co. and B Co. were related parties during June and December but there were transactions among them between January and December of the same accounting period. Inter-company transactions only for the period when the relationship in accordance with Section 71 bis Clause 2 occurred should be disclosed in the TPDF.

- For the MNE group with a foreign ultimate parent entity (“UPE”), the threshold for preparing/ submitting the Country-by-Country Report (“CbCR”) should be based on the CbCR regulations/ requirements in the country where the UPE is a tax resident.

PKF Thailand’s observations

In the above example, the consideration of related parties does not take into account only the shareholding proportion of each individual shareholder, but the TRD also considers the shareholding ratio of the same “group” of shareholders. Over the past month, we have seen a trend in TPDF audits following this interpretation of the TRD. Therefore, taxpayers should carefully review their lists of related parties to determine which companies are also classified as related companies under this new interpretation.

Please let us know if you have any questions or concerns. Our Transfer Pricing professionals at PKF Thailand would be happy to assist.