Welcome to the February 2023 edition of Tax Times Thailand where each month we try and bring you useful information to help with your business and tax obligations in Thailand.

“T’was the night before Chinese New Year, and all through the house, Not a creature was stirring, except Personal Income Tax Departments all around Thailand!!”

Gentle Reminder

If you were resident in Thailand for 2022 (i.e., you were physically here for 180 days or more in 2022), and you have assessable income over THB 60,000 or THB 120,000 (depending on the type of income),

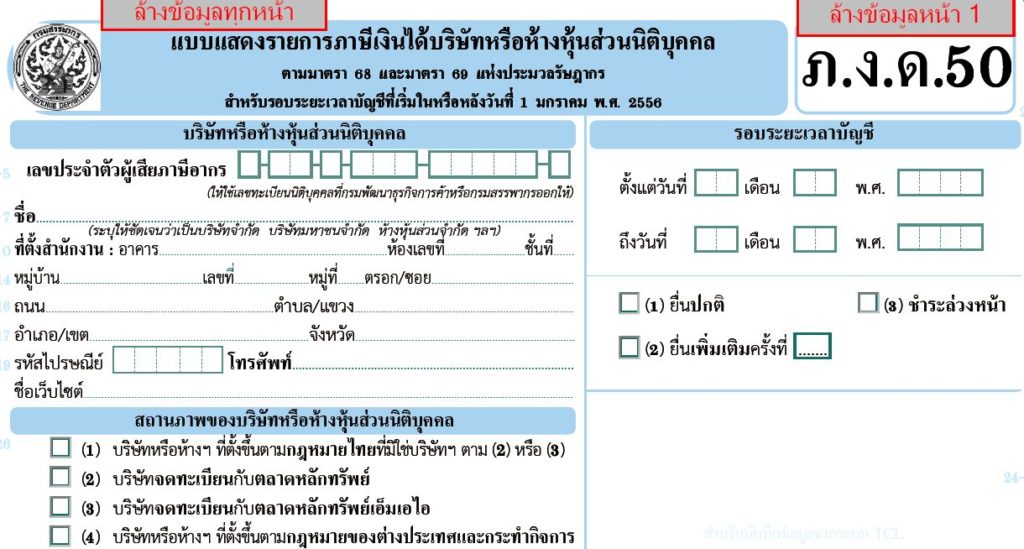

please ensure that your Personal Income Tax Return (PND 90 or PND 91) is completed and submitted to the Thai Revenue Department (TRD) by31 March 2023 (or by 10 April 2023 if you are to make the submission via the internet).For companies with a 31 December 2022 yearend, following the statutory audit, the final corporate income tax return (PND 50) should be completed and submitted to the TRD by 30 May 2023 (or by 7 June 2023 if you are to make the submission via the internet).

(In addition, for companies with a 31st December 2022 year end, the SBC3 submission (audited financial statements and list of shareholders as at the date of the AGM) should be made by31 May 2023 (or by 8 June 2023 if the submission is to be made via the internet).

From 7 February 2023, the Civil and Commercial Code of Thailand will recognise the concept of ‘merger’ in addition to amalgamation. Legally, this is a significant step forward for the ease of joining or ‘merging’ companies in Thailand.

Under the existing ‘Amalgamation’ rules, if Company A wishes to join with Company B, a new company C must be formed to ‘house’ the combined operations and the ‘empty’ shell companies A and B must both then be liquidated.

Under the new ‘merger’ provisions however, Company A and Company B can now legally merge operations i.e., A into B or B into A with one entity (either A or B) becoming the prevailing surviving entity going forward and taking over the absorbed company’s assets, rights, and liabilities. There is no liquidation process or liquidator required for the non-surviving company left behind and it simply ceases to be a ‘juristic person’ recognised under the law. Further, in the merger process, unlike amalgamation, there is no requirement to create a third company to ‘house’ the combined business operations as this absorbed into the surviving company’s operations.

The current provisions of Thai Revenue Code (‘TRC’) recognize two forms business combination:

– Amalgamation (where two or more companies combine and become a new company) under Section

74 (1)(b) TRC; and,

– An entire business transfer (where a company transfers its entire business to another company, and it

is then dissolved in the same accounting period) under Section 74 (1)(c) TRC.

Against this background, it is yet to be confirmed if, and under what circumstances, a merger business

combination can be covered by one of the tax provisions of Section 74 TRC.

In summary, the new company merger provisions allow a different combination route for companies and can provide a more efficient process. However, there are still some ‘grey areas’ where guidance and direction is required from the authorities.

To merge or not to merge–that is the question?

Tax notes

VAT Refunds – update

VAT refund applications with the Thai Revenue Department (TRD) generally take approximately

one year (assuming a basic Tax Audit is also undertakenby the TRD) depending on the size of

the claim and availability of requested documentation i.e., from making the initial refund

application to receiving the refund (and registering PromptPay). We have found however that

it can go a lot quicker with regular interaction with the Thai Revenue Officer (TRO) and ensuring

any information and documentation requested is properly prepared and complete.

Withholding Tax Refunds – update

Withholding Tax (WHT) deducted at source from payments made to a Company is normally

relieved by claiming it against the annual corporate income tax (CIT) payable in the same year.

Where, however, the amount of WHT exceeds the annual CIT payable and surplus WHT arises;

it cannot be carried forward to relieve future CIT payable but has to be recovered by way of a

refund application using form PND 50 or Form Kor10.

WHT refund applications with the TRD generally take approximately one year depending on

the size of the claim and availability of requested documentation (assuming a basic Tax Audit

is also undertaken by the TRD) but sometimes this time is extended where different TRO’s

handle different claim years. Withholding Tax refund applications can be significant and so it is

very important each claim is made within the 3-year limit otherwise the amount will be lost.

It may be the result of emerging from Covid, and more TRD staff being back at work, but we

have noticed both VAT and WHT refund applications generally being handled quicker.

The Multilateral Convention – update

On 9 February 2022, Thailand signed the Multilateral Convention (‘MLC’) to implement certain

OECD Base Erosion and Profit Shifting (BEPS) measures which then apply to Thailand’s Double

Tax Agreements (‘Tax Treaties) with countries which have also signed up to the MLC. In practice

we have not yet seen any impact of this yet on our clients, although we appreciate it is still ‘early

days’.

Transfer Pricing – update

For companies in Thailand with related parties and an annual revenue of THB 200 million or

more in an accounting period, Section 71 ter TRC sets out requirements for the completion of

a Transfer Pricing Disclosure Form (TPDF) and empowers the TRD to request additional transfer

pricing documents or evidence necessary to analyse the related party transactions. Notably, we

have seen a strong increase in the number of companies requesting assistance with filing TPDF‘s

and completion of Transfer Pricing Local Files, sometimes for several years – we have not

however seen a similar increase in Country-by-Country reporting and Master File requests.

Submission Deadlines – February 2023: Tax Returns and Forms

FEB

7

Por Ngor Dor 1 (PND 1)

[Remuneration paid to employees by Company]

Report: Monthly withholding tax deduction from remuneration paid to employees (in January 2023).

*Due by 15-Feb-2023 if submission via internet.

Por Ngor Dor 2 (PND 2)

[Dividend payments made by a Company]

Report: Monthly withholding tax paid on dividends (in January 2023).

*Due by 15-Feb-2023 if submission via internet.

Por Ngor Dor 3 (PND 3)

[Domestic payments by a Company to individuals]

Report: Monthly withholding tax deduction from

payments made by a Company in January 2023 for consulting services, rent, hiring freelancers, transportation, insurance, management fees, etc., to individuals in Thailand.

*Due by 15-Feb-2023 if submission via internet.

Por Ngor Dor 53 (PND 53)

[Domestic payments by a Company to a Company]

Report: Monthly withholding tax deduction from payments made by a Company for consulting services, rent, hiring freelancers, transportation, insurance, management fees, etc., to a Company in Thailand (in January 2023)

*Due by 15-Feb-2023 if submission via internet.

Por Ngor Dor 54 (PND 54)

[Payments by a Company to a foreign Company]

Report: Monthly withholding tax deduction by a Company from an amount paid in or from Thailand in respect of a post or the performance of work, goodwill, copyright, any other rights, software, royalty, license fee, interest, dividend, rent, professional fees, share of profits or any other gain to a foreign Company not

carrying on business in Thailand (in January 2023).

*Due by 15-Feb-2023 if submission via internet.

Por Por 36 (PND 36)

[VAT Return -imported goods / services and certain

non-Thai resident supplies]

Report: Monthly VAT Return for input VAT on imported goods or services and for services used in Thailand supplied by foreign service providers under Section 83/6 Thai Revenue Code (‘TRC’) in Jan-2023.

*Due by 15-Feb-2023 if submission via internet.

FEB

15

Por Tor 40 (PP 40)

[Specific Business Tax (SBT) Return under Section

91/10 TRC]

Report: Monthly SBT Return for Jan-2023 by SBT Registrant operating business of banking, credit foncier, finance, life insurance, pawnbroking, securities, and regular transactions similar to commercial banking.

*Due by 23-Feb-2023 if submission via internet.

FEB

23

- Por Por 30 (PP 30) if submission via internet.

- Por Tor 40 (PP 40) if submission via internet.

Por Por 30 (PP 30)

[Value Added Tax (VAT) Return]

Report: Monthly VAT Returnshowing output VAT, input VAT and net VAT position (for Jan-2023) by a VAT registrant. If net output VAT, remit payment.

*Due by 23-Feb-2023 if submission via internet

- Por Ngor Dor 1 (PND 1) if submission via internet.

- Por Ngor Dor 2 (PND 2) if submission via internet.

- Por Ngor Dor 3 (PND 3) if submission via internet.

- Por Ngor Dor 53 (PND 53) if submission via internet.

- Por Ngor Dor 54 (PND 54) if submission via internet.

- Por Por 36 (PND 36) if submission via internet.

FEB

27

Transfer Pricing Disclosure Form (TP Disclosure Form)

Report: Annual TP Disclosure Form for Company with annual turnover > THB 200 million and related parties with a year end 30 September 2022.

*Due by 7-Mar-2023 if submission via internet.

Por Ngor Dor 50 (PND 50)

[Annual Corporate Income Tax (CIT) Return]

Report: Annual CIT Return for a Company with an accounting year end 30 September 2022.

*Due by 7-Mar-2023 if submission via internet.

FEB

28

Por Ngor Dor 51 (PND 51)

[Mid-year Corporate Income Tax (CIT) Return]

Report: Mid-year CIT Return for companies with an accounting year end 30 June 2023.

*Due by 8-Mar-2023 if submission via internet.

MAR

7

- Transfer Pricing Disclosure Form (TP Disclosure Form) if submission via internet.

- Por Ngor Dor 50 (PND 50) if submission via internet.

MAR

8

- Por Ngor Dor 51 (PND 51) if submission via internet.

- Sor Bor Chor 3 (SBC 3) if submission via internet.

- Por Ngor Dor 1 Kaw (PND 1 Kaw) if submission via internet.

Sor Bor Chor 3 (SBC 3)

[Audited financial statements + list of shareholders]

Audited financial statements of a Company with an

accounting year end 30 September 2022and list of shareholders as at the AGM date (31-Jan-2023).

*Due by 8-Mar-2023 if submission via internet.

Por Ngor Dor 1 Kaw (PND 1 Kaw)

[Remuneration paid to employees by Company]

Report: Annual summary report on withholding tax deducted from remuneration paid to employees (in 2022).

*Due by 8-Mar-2023 if submission via internet.

click here to share this